Definition Of Equity Under Ifrs

Ifrs 9 Stages Of Risk Financial Management Risk Management Financial Accounting

Principles Of Group Accounting Under Ifrs Paperback Overstock Com Shopping The Best Deals On Accounting Accounting Principles Education Jobs

Lease Accounting Treatment By Lessee Lessor Books Ifrs Us Gaap Financial Strategies Cash Flow Statement Financial Management

Lease Accounting Treatment By Lessee Lessor Books Ifrs Us Gaap Accounting Cash Flow Statement Financial Management

Us Gaap Vs Ifrs Bookkeeping Business Accounting Education Accounting And Finance

Financial Assets Under Ifrs 9 Bdo Nz

And certain instruments that are equity under ifrs could be classified outside equity under us gaap.

Definition of equity under ifrs. International accounting standards ias 1 suggests that shareholders interests be subcategorised into three broad subdivisions. They are puttable instruments ias 32 16a and 16b. Capital structures can be complex containing a number of features and performance characteristics. The term equity is often used to encompass an entity s equity instruments and reserves.

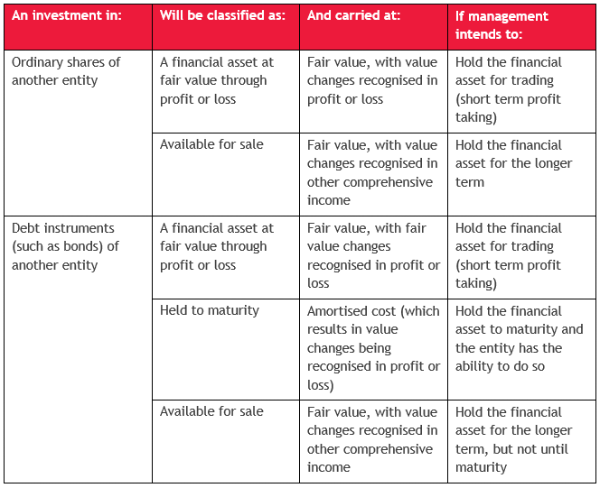

Within scope out of scope debt and equity investments investments in subsidiaries associates and joint ventures loans and receivables. Shareholders equity is comprised of all capital contributed to the entity plus retained earnings. As a result some have suggested that the board consider changing the requirements in ifrs 9 for equity investments. Against that background the european commission called for close monitoring of the impact of ifrs 9 on long term investors and asked efrag to investigate the potential effects of the requirements in ifrs 9 for equity investments.

Equity is defined as any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities ias 32 11. Ifrs 2 share based payment requires an entity to recognise share based payment trans ac tions such as granted shares share options or share ap pre ci a tion rights in its financial state ments including trans ac tions with employees or other parties to be settled in cash other assets or equity in stru ments of the entity. Equity is defined in the iasb s framework as the residual interest in the entity s assets after deducting all its liabilities. A ias 1 presentation of financial statements b ias 8 accounting policy changes in accounting estimates and errors c ias 16 property plant and equipment d ias 21 the effects of changes in foreign exchange rates e ias 38 intangible assets.

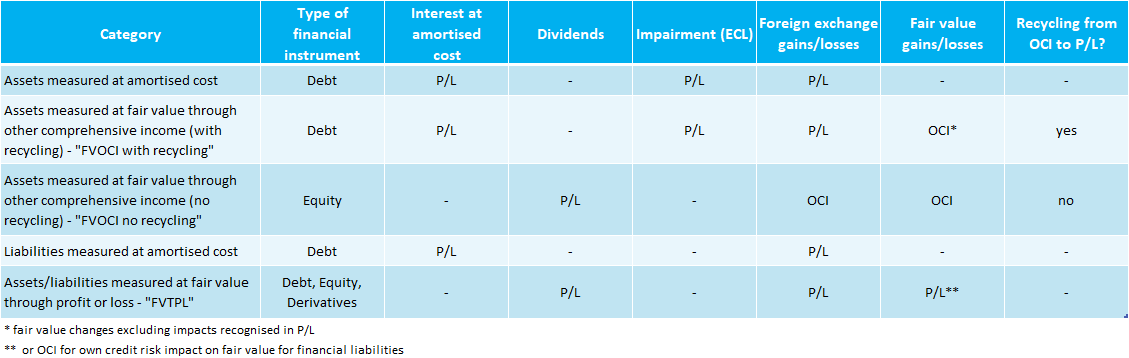

Equity is given various descriptions in the financial statements. 4 financial instruments under ifrs scope the scope of the standards is wide ranging. Equity or commodity indexed interest or principal payments embedded in a host debt instrument or insurance contract are by definition not closely related to host and therefore should be separated ifrs 9 b4 3 5 c d. Issued share capital retained earnings and other components of equity.

Equity there is no ias ifrs for equity requirements for measurement and disclosures.

Classification Of Financial Assets Liabilities Ifrs 9 Ifrscommunity Com

Ias 39 Financial Instruments Recognition And Measurement This Summary Speaks About Ias 39 Replacement B Financial Instrument Financial Financial Engineering

An Indian Ifrs For Accounting Of Employee Benefits Timelines For Implementation Of The Indas19 Employee Benefit Accounting Period Accounting

Ifrs 9 Business Model And Sppi Testing In 2020 Financial Asset Time Value Of Money Financial Instrument

Three Statement Model Practical Example Of Tsm Ifrs Vs Us Gaap Money Management Advice Cash Flow Statement Accounting And Finance

Ifrs Vs Us Gaap 6 Major Differences You Should Know Cash Flow Statement Financial Statement Income Statement

Getting Ready For Ifrs 9 Accounting Standards Bloomberg Professional Services Risk Management Accounting Accounting Career

Small Business Accounting Archives Mirex Marketing Small Business Accounting Accounting Accounting Classes

Ebitdarm Meaning Importance And Shortcomings Economics Lessons Financial Life Hacks Accounting And Finance

Wiley Interpretation And Application Of Ifrs Standards 2019 Ebook Ebook Details Author Pkf Internati Interpretation Download Books Book Recommendations

Gaap Vs Ifrs What S The Difference And Which Should You Use Hbs Online

0rsa5sgqybpbfm

Ifrs 16 Leases Vs Ias 17 Leases How The Lease Accounting Changed Ifrsbox Lease Accounting Change